Panthera Update

What the latest RNS actually means for us investors, and a complimentary lesson to go with it. Double whammy.

There’s not much to say here, but for those that missed the RNS today or are looking to fulfil their confirmation bias (feel free). We have also attached some procedural theory to help you manage expectations…

Our Analysis can be found here on Substack:

Or over on our website: https://www.case-research.co.uk/panthera-resources

Speculation

There’s been more than the fair share of speculation around when India would file their counter-memorial. They now have, and we can’t see it yet.

But why?

It was a key contingency on the case moving forward, and you can tell a lot about the Respondent (India) by how timely they are. If they file right on the deadline, you could read it one of two ways:

They were as prepared as possible

It was a strategic lateness, or they were scrambling till the last minute

Of course, there’s now way of knowing until at least the hearing has been made public, if that, but considering that including settlements claimants like Panthera win arbitrations over 50% of the time, you can err with optimism.

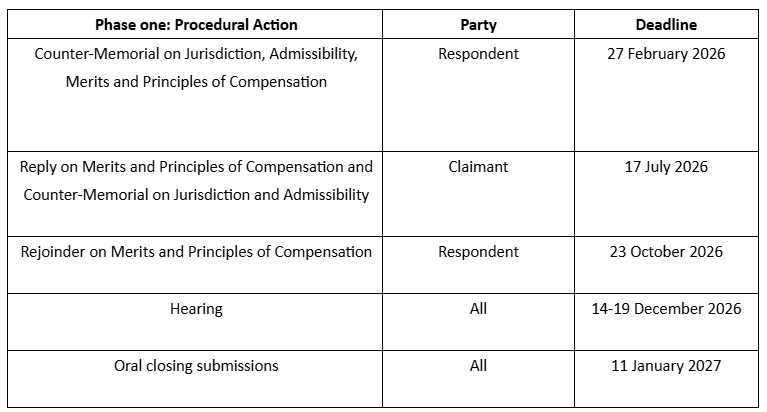

What’s next

We have had the counter-memorial ‘confirmed’ by the company after it’s announcement on October 29th last year:

You can think of this as the ‘full evidentiary hearing phase’ (a common term). You will also notice it says ‘Phase One’, implying there are more.

So what happens at the close of this phase?

Well, the next procedural order hasn’t been released, naturally, but as usual the Tribunal should deliberate on the submissions content, and may issue a partial award in relation to whatever issues they find, e.g. liability or jurisdiction. If jurisdiction is upheld, the case can move forward, and if liability is found, they can begin discussing the Quantum / Damages phase. If we get that far, let’s hope it’s more efficient, and generally less painful, than the Winshear hearing:

[I bring this up to show how informal governments can be, and generally ill prepared. You can guess who won the case via settlement… (we feel neutral toward the case, personally speaking, and have nothing against the figures presented in this case / related affairs)]

Then comes the hearing on quantum, the following briefs (if ordered), and the final award.

So how long until the decision: Well, at least three years, but the Phase 2 procedural order will lay out that path as the current one has done for us, albeit possibly subject to change.

The incredibly counterintuitive tendency you need to throw away to become a better arbitrations analyst, and you’re probably falling for it -

Arbitration investors, as any fool could spot, are a largely speculative bunch. They all get in the habit of asking ‘how does this affect the case’ or ‘how will the price react to this?’

But what’s wrong with that? They’re rational questions right? I need to know how my thesis changes?

And, while technically yes, it ignores two very crucial elements: complex systems, and non-public information....

Complex system: investors may know this as the whole > sum of the parts, which is a good enough definition practically speaking.

Non-Public information: well, we all know what that is

So, while these questions are natural, analysing the legal case at each update, in depth, is only useful for guessing the direction things will go. Not a precise end point. You cannot assign a direct probability to something, and even if you could you shouldn’t, because the tribunal is going to take the update following the most recent one and overlay it with the rest of the facts to interpret. Sure, you can think it’s worth X at Y time and so the price should adjust, but in these situations you hold around the time of decision - it’s when the value is most certain, and historically when most of the returns come. However, as each set of facts could change the Tribunal’s view on the others, you can only assess if the sum of the parts (the updates) is greater than the whole once the decision has been made. You can only use general statistics in assigning value to the case - never say ‘Panthera is worth X% of the claim’ until the award has actually been paid. Remember, even after the decision, there’s still the possibility of annulment, and likely need for enforcement - the one thing arbitrators keep telling me is ‘to never assume the state will pay’.

Then there’s the private aspect, away from prying eyes like us Substackers. Bribery. Tactical flower sending to the opponents wives. Threats. You name it, it’s been done before, and more than once across cases. While everything that happens under the eyes of the tribunal, at least the vast majority of the time, is out in the open, you still have the world of personal relations between e.g. Panthera and India. This is not an accusation, but is getting you to consider that not everything is always particularly procedural - humans are biased by nature. We can’t avoid that. Then there’s the relationship between the Arbitrators, which has biases of it’s own e.g. you may not want to issue a dissenting opinion, even if in favor of whoever appointed you, because you don’t want to be seen as having the wrong ideas, or whatever they conjure up.

So you put these two ideas together, and you get the best way to invest in Panthera: buy with such a statistically large margin of safety, which any buyers now have, such that those two problems don’t actually matter.

So if a precise valuation is only clear retrospectively, but I don’t want to hold for years until the decision, what do I do?

Well, you sell and come back to it later - the majority of returns in arbitrations come from the 6 - 12 months around the tribunal decision, which only goes to prove our point in the last section.

If you have your finger in a few (arbitration) pies, do as any good investor does: look at the CAGR and the risk/return. There is no point owning a case concluding in five years if there’s no reason for it to appreciate for the next four, when your downside is still 100%. There’s also no point holding onto a claimant you’re 500% up on if the downside is still 100% and you’re unsure about the decision. Basically, if the expected return in X period is poor compared to the downside potential, sell for now or at least trim your position.

Take a look for yourself…

RNS Link: https://www.londonstockexchange.com/news-article/PAT/arbitration-update/17481587