The Case Research Portfolio

Names, proportions, upside, and timeline of every stock I own

Primer -

We feel this is fairly self explanatory, but we are writing this piece for two reasons. First, so you know our highest conviction positions, and what we expect of them, and second, because we realised that we should specify: we do not own everything we research!

We are a research firm, and while we do only write about positions we believe in, we do not see the use in owning all of them when we could just own the few best risk/return tradeoffs (considering the downside is often 100% in these scenarios, it’s mostly just the highest upside ideas). Of course, we take time into account too, and will continue to adjust our positions as we see the odds of the thesis / how it plays out changing, as any responsible investor does.

My portfolio is split into two sections - Arbitrations and Resource Investing. Whether a coincidence or not, as a class, junior miners find themselves disproportionately present in international arbitrations relative to other industries. This could be due to the capex heavy nature of junior mining operations making the managers of those business more incentivised to seek compensation than a toll-booth business (for example).

Arbitrations: As my readers will know, I specialise solely in publicly listed companies involved in any stage of an international arbitration. Most often, this involves a company who has had their operation discontinued in some way in an unfair manner without compensation, most often by a government. You’ll hear the word ‘ICSID’ a lot, which is the centre for the settlement of these issues between e.g. a UK-registered / owned business operating in Morocco and the Moroccan Government. Most of my time is spent trying to figure out if the claimant (business) has any legal standing, what are the chances of each outcome, and how long this all might take. There’s other things too, like if the business’s case is being funded by someone with a great track record in these situations, or what the management may do with the award (dividend or reinvestment). That’s what it all comes down to - an award, AKA compensation owed under the treaty between e.g. the UK and Morocco (to keep the example going). Once I’ve figured out the expected value (probabilities) of the businesses compensation, I weigh it against the market cap and see my upside, risk/return, and margin of safety. My writeups lay out this process, but that’s the short answer. I am a massive fan of arbitrations for a few reasons:

1) attractive risk/return tradeoffs: the business is treated as if it has lost its operation, and they ignore the legal claim, which puts the market cap practically at zero, and so we get the legal case as a free option on value creation. I typically see 1:5-20 risk/return tradeoff ratios.

2) probabilities: the odds are fairly easy to calculate, and if unsure, use historical averages of similar cases, which is a great benefit of the law being so procedural - comps are simple. Even ICSID cases generally have a 56% win rate, or you can expect 18% of what the company wants on average if you account for failure rate. A company I recently looked at has 1000% upside to ICSID averages, assuming a probable positive outcome. This is not uncommon in the right places, especially for early stage cases.

3) predictable timelines: that procedural nature means you can estimate a range for the time until compensation

4) Multiple catalysts: as each new case submission is made, the market has a new chance to realise the awards expected value, and the stock should follow

5) Minimal assumptions: legal cases are incredibly fact-based, and so there’s very little left for guesswork. If you’re ever unsure, there’s a torrent of legal information / studies out there which help figure it out, and so you never need to assume much. Especially for legal cases. Of course, if you do assume, be incredibly conservative.

Resources: as my readers will know, I’m not a resource analyst, but my business partner Case Resources is. He’s been focusing on mining since he was 15, and he’s only gotten better. Obviously, I’m biased, but he’s the best mining analyst I know. Whether you’re an investor, mining company manager, or a school janitor, I highly recomend checking him out: https://substack.com/@caseresources

To distinguish between the two, I will start off with arbitrations (my work) and then move on to his, followed by the joint performance I expect.

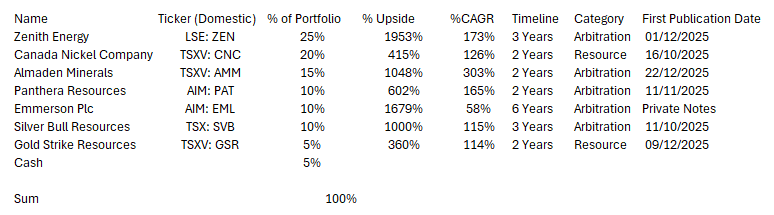

Total Portfolio

[Data is as of publication]

Note: All our estimates are conservative (expected value, so accounts for probabilities, which we are pessimistic with), and there’s significant margin across the board, but if wondering why we don’t more money (proportionally) towards higher CAGR ideas, it’s because we were more conservative with some and not others. There’s also other factors, like if we’ve talked to the management or if other competent people are invested.

Expected Performance

Weighted by % of that portfolio’s section, either Arbitration or Resources, the expected performance is as follows:

Arbitrations (70%): 174% CAGR (2-6 years)

Resources (25%): 123% CAGR (2-3 years)

Cash (5%): 0% CAGR —> inflation —> negative CAGR —> assume 0 for simplicity

So, that’s 153% per year if holding all names mentioned.

Addressing Skepticism: High Return Ideas are ‘Sketchy’

Especially when talking to investors not involved in these niches, we often get something like ‘seems a bit optimistic’ or ‘you must be being very aggressive in your assumptions’, and while we understand the concern, we have some thoughts…

Arbitrations/junior miners are two pockets of the markets which are highly inefficient, but only currently. How would value investing work if markets were inefficient forever? As to why these discounts exist, you can ask Case Resources about the miners, but I can speak for arbitrations. The discounts mostly exist because of a very general factors that apply to all situations, above all shareholder turnover - imagine you own stock in a junior mining company, and all of a sudden (can be dragged out, however) this company loses all economic exposure to the project, so you have no idea how to value the stock whose value now depends on a legal case. What happens then? You sell, often desperately, which pushes down the price, and then the stock is left for dead for a year or two (at least) before the arbitration investors notice it. If questioning why the arbitration investors don’t snatch these cases up immediately, it’s 1) because they’re typically very conservative, and 2) are patient - they would rather wait for the case to progress and the expected value of the award to become clearer before taking a position. You do get a small crowd, us included, who will think of early stage cases as statistical bets and go off historical averages, like how we assume the S&P will continue doing 8-10%, and then adjust our position as more info is revealed. We will of course not invest in a case where we can’t get a judgment on the principle, at least, so it’s not a shot in the dark. Like all good investments, some things are just obvious. It is only later that the stock typically gets recognition, making the returns very late-weighted. You may have two years of flat/negative returns, at which point you buy more (if you’re still convicted), and then on that third year all the catalysts e.g. a hearing occur.

How our portfolio will change:

Like most microcap investors, as these often are (mostly below $100mn), they are worth keeping an eye on. Our verdict on the thesis is often self-challenged, and it rarely changes, but there’s other things to look out for such as volume - if the AMM thesis, for example, plays out and it’s now 50% of my portfolio, it’s not worth anything if you can’t sell. Stocks only hold their value insofar as what they’re worth when you sell, otherwise there’s nothing you can do with them. This doesn’t mean you shouldn’t look for long term investments - we have spent the vast majority of our years on the lookout for such opportunities, but when working with small sums there’s more discounts you can exploit on the special situations side of things. Buffet has talked about his scaling problem in great detail - greater returns on invested capital are generally generated in lower market cap businesses. Multiple studies have noted micro/small-cap outperformance.

Now that we have that in mind, unless we magically come across a very large sum, arbitrations will remain the focus here at Case Research, but our circle of competence goes beyond arbitrations - we have spent many years, especially our teens, going over discounted Berkshire style situations (competitive advantages, predictability, management, and all of the classics), deep value (mostly catalyst-driven basket approach - we liked Japan as our initial hunting ground as 60% of stocks there sold below book), and special situations (liquidations / preferred stock arbitrage mostly, which we know is an odd combo, but we focus on what we know and what works). You should be weary of having a wide circle of competence, but we stick to anything we find simple enough to not require many assumptions (and preferably none, which is rarely the case). This range over the years has given us a fairly wide mental framework, and we continue studying other areas, whether it be immune system / inflammatory response (a current focus), developmental psychology, or biographies. The multidisciplinary approach is unlikely to go out of favor with us.

In terms of our actual positions, which is probably what you’ve been waiting for, we only sell a stock for two reasons: 1) we have found a better time-adjusted risk/return, or 2) the stock has reached it’s fair value. It could be both, of course. However, considering the multi-year timeline, and the limited choice in the arbitration space, we think it’s unlikely positions will be sold out of completely. What we almost definitely will do is adjust the position as the cases progress - with each new submission, we can reassess the situation / it’s value, and adjust accordingly. What would be the point of having an idea with 100% upside to fair value left if it takes two years, but there’s a 70% upside idea in one? It’s about the time-adjusted returns!

Then there’s the resource investing, and I would trust Case Resources implicitly to run that part of my portfolio, or more aptly, for me to copy him. We are business partners, and so often consult on ideas regularly - our informal debates have been known to get heated from time to time.

Why I own each name: analysis snippets

You’re probably wondering why each of these names is attractive, and it’d be cruel not to give you any justification. Our research can be found on our respective pages, and if we wrote a summary, they’re there too!

Zenith Energy

Bottom line, their operating business is worth at least the MC, and their legal claim portfolio trades at 5% of fair value if you write off the op business. The discount exists because they lost an unrelated case in June, and the stock dropped 75% in one day and hasn’t been reconsidered since. We see 2000% upside in five years to the probability weighted awards, and full downside protection from the operating business.

Canada Nickel Company

Almaden Minerals

Almaden Minerals (TSXV: AMM) is in ICSID proceedings with Mexico over a gold and silver mine concession which was revoked, which is an expropriation-rich jurisdiction with clear proof of the CPTPP-breaching mining law changes. The memorial is extremely convincing, as it was with Silver Bull Resources (SVB.TO).

AMM offers 1048% upside in two years, trading at 8% of the awards expected value (including risk of loss). The hearing is scheduled for the end of 2026, so an award is likely by August 2027, or 360% CAGR. This is essentially risking $1 for $22 of upside if you factor in the probabilities.

Being initiated in 2024, the proceedings are early stage, but even at ICSID averages it should trade at c.18% of the claim, or over 100% upside before anything’s actually happened.

Another great lever on returns is the gold and silver price, which have both appreciated about 250% since the memorial, which leaves you with a 3,668% upside. However, it’s not entirely clear if this was included in the recent memorial, so take it with a pinch of salt. Of course this could change, and the leverage goes both ways, so the 1048% figure is what we officially think, but technically it’s the correct figure as of today.

The discount largely exists due to a very slow shareholder turnover, the $18mn market cap, and pessimism regarding the risks: unfavorable ruling, enforcement issues, and possible poor cash allocation from the management post award payment.

Panthera Resources

After India blocked Panthera’s prospecting license for Bhukia, a 75% owned JV, Panthera tried to resolve in Indian High Courts, but was forced to take to the Permanent Court of Arbitation on the basis of expropriation under the Australia-India BIT. India had passed a decree to effectively nationalise the mining industry, and claimed that Bhukia wasn’t a sound project anyway, despite later auctioning it off to a domestic company. Panthera argued breaches of Article 3 (promotion / protection of investments), 4 (treatment of investments), and 7 (expropriation and nationalisation). It’s evident all were broken...

However, the case hasn’t reached the hearing, and procedure keeps arguments private, making it hard to judge the outcome with any certainty, but it has LCM’s backing, who have a 80%+ win rate over 13 years. Certainty, however, isn’t needed - Panthera claim $1.5bn, but we came to a $577mn award vs a $82mn market cap, giving 602% upside (165% CAGR) in two years (procedural order). Management intend to issue a special dividend and then give shareholders the chance to reinvest which is a thoughtful optionality.

This discount is thanks to incredible market pessimism, shown by the implied probability - they value Panthera at a 14% chance of receiving the $577mn, which is too low for an already conservative estimate. This gives us great leverage on small mental adjustments the forward-looking market will make as the case progresses e.g. the market deciding it’s a 25% probability instead gives a 78% price appreciation. It could go either way, but case info being made public can be an excellent catalyst, along with the eventual award.

The risks here are that Panthera receive no award, lower annualised return as the tribunal have to delay their decision thanks to India-related delay attempts, Panthera poorly allocating the cash to their two Mali and two Burkina Faso projects, and the market somehow never recognising the value. However, these are individually improbable.

If looking to take a position, if you understand the key value levers: how right Panthera are on principle (assessable now), if India have any legal standing, and the tribunals eventual decision, then you should make the position in the upper quartile of what you’d normally allocate. If just making a blind bet, which we find nonsensical, then it’s up to you, but considering the two year timeline / sizeable upside we’d have it as a small position. We do, however, recognise that it depends on your risk tolerance and personal situation, so adjust accordingly.

Initial Coverage: https://caseresearch.substack.com/p/panthera-resources-lse-pat

CEO Talk (Takeaways): https://caseresearch.substack.com/p/panthera-lsepat

Overview: https://caseresearch.substack.com/p/the-daily-dispute-3-panthera-resources

Emmerson Plc

I’ve kept the writeup private, but here’s the summary:

- ICSID Case (Emmerson Plc v Kingdom of Morocco, Case # ARB/25/22)

- Dispute: rejection of environmental/social impact assessment; water usage concern

- RFA: 23rd May 2025

- Emmerson Water Efforts: capex heavy reductions to get usage down 50%; multiple rejections followed

- Morocco’s over conservatism: Emmerson would only use 0.6% of reserves; pos. socio-economic / water usage tradeoff

- Rejections: multiple rounds; no progress; ICSID responsible choice

- Incentives: Morocco’s is unclear; Emmerson’s water planned not otherwise allocated

- BIT Breach: lack of fair and equitable treatment clear; includes lacking compensation on/before expropriation date

- Parties Track Record

- Emmerson arbitrator: 93% of wins (appointing side W/ favorable outcome) while representing claimant, and 62% overall

- Emmerson backing: BSF / Tim Foden, who is a highly competent lawyer with a great track record

- Moroccan legal counsel: 1/3 win rate, only done three cases, and arbitrator has 57% win rate, with all losses while representing the state

- Incentives: Emmerson’s litigation funding is non-recourse; (unrelated) some tribunal inter-personal bias inevitable, so not wholly rational / fact based outcome

- Valuation (US$)

- Award P/S (prob weighted; net of liabilities): 0.53

- Price P/S: 0.03

- Target P/S: 0.53

- MC($Mn): 42.00

- Upside: 1679.30%

- CAGR: 58% (6 years)

- Risk / Return: 1/17

- Margin of Safety: 85% reduction in award estimate --> 1:3 risk:return tradeoff

- Allocation: future dividend unclear, likely at least in part

- Catalyst: case progression gives many, periodic, chances to make odds / EML’s fair value more apparent

- Risks

- Bear Case: Loss

- Potash Price Leverage: compensation (award) based on project value, so Potash price leverage

- No monetary award: no other value driver currently

- Enforcement trouble: ICSID ruling doesn’t equal forced payment; another proceeding required

- Poor award allocation: if new project pursued, a poor project would warrant a lower valuation; no guarantee if up/down post-award date

- Reason for discount

- Shareholder turnover: junior mining investors out, new arbitration holders need time to assess

- Ignorance

- Single value driver: dependence on case may drive conservatism, at least for now

- Niche: arbitrations, especially early stage, are not as popular as e.g. Buffet’s style

- Volume: £25k per day ($32k) rules out many funds / competent investors. Same for Market Cap.

Gold Strike Resources

I was thinking of the method you follow. Basically you anchor your expectations and math on historical arbitration data. Thats a good starting point to calcaulations, and could be more softened by chosing the seemingly best cases (as all case is different from many aspects) although the legal bases are always hard to assess for a layman. That said, this statistical approach can be work if you also have many cases (stocks) in the portfolio to let the likelihood/math work.